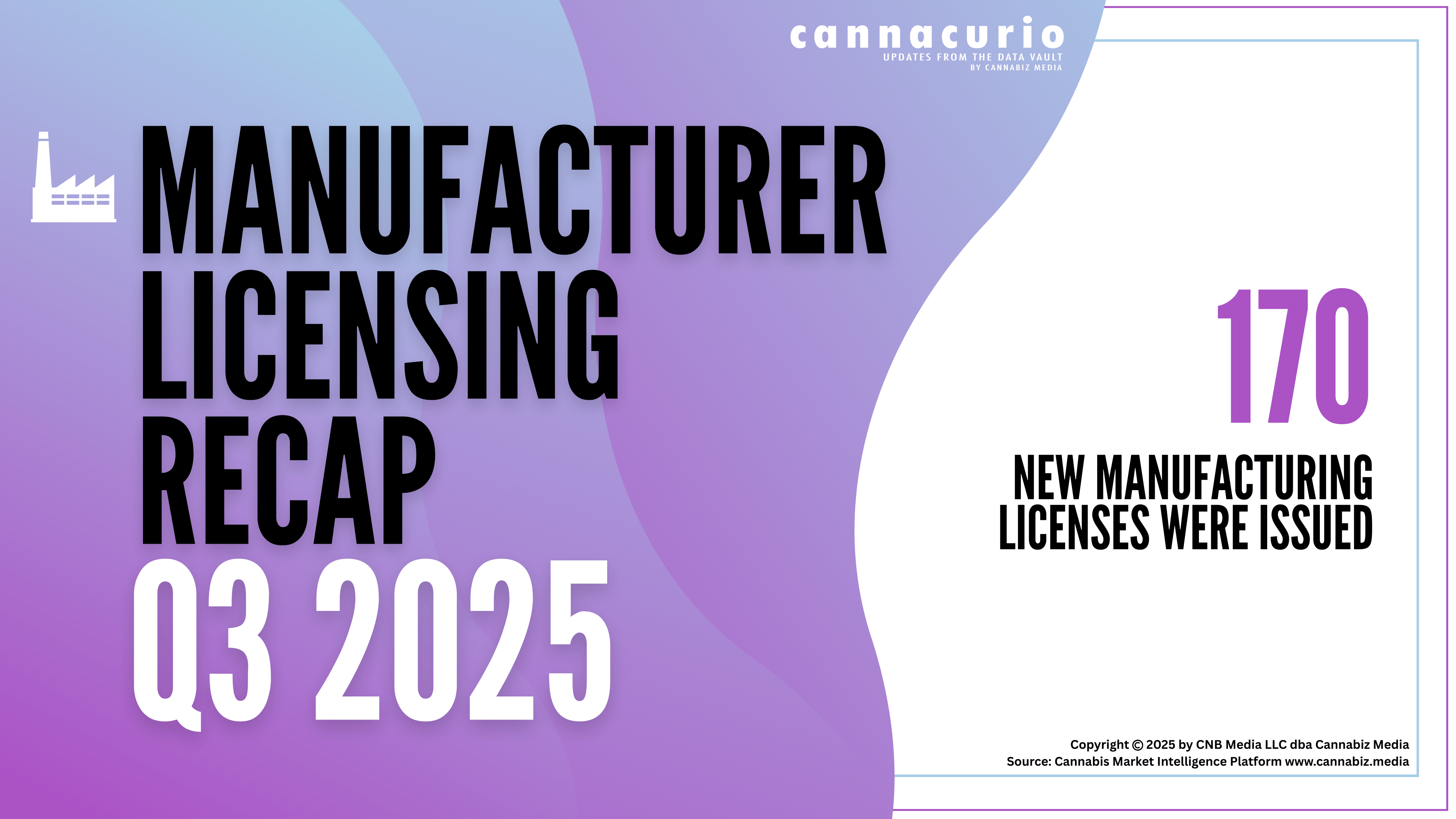

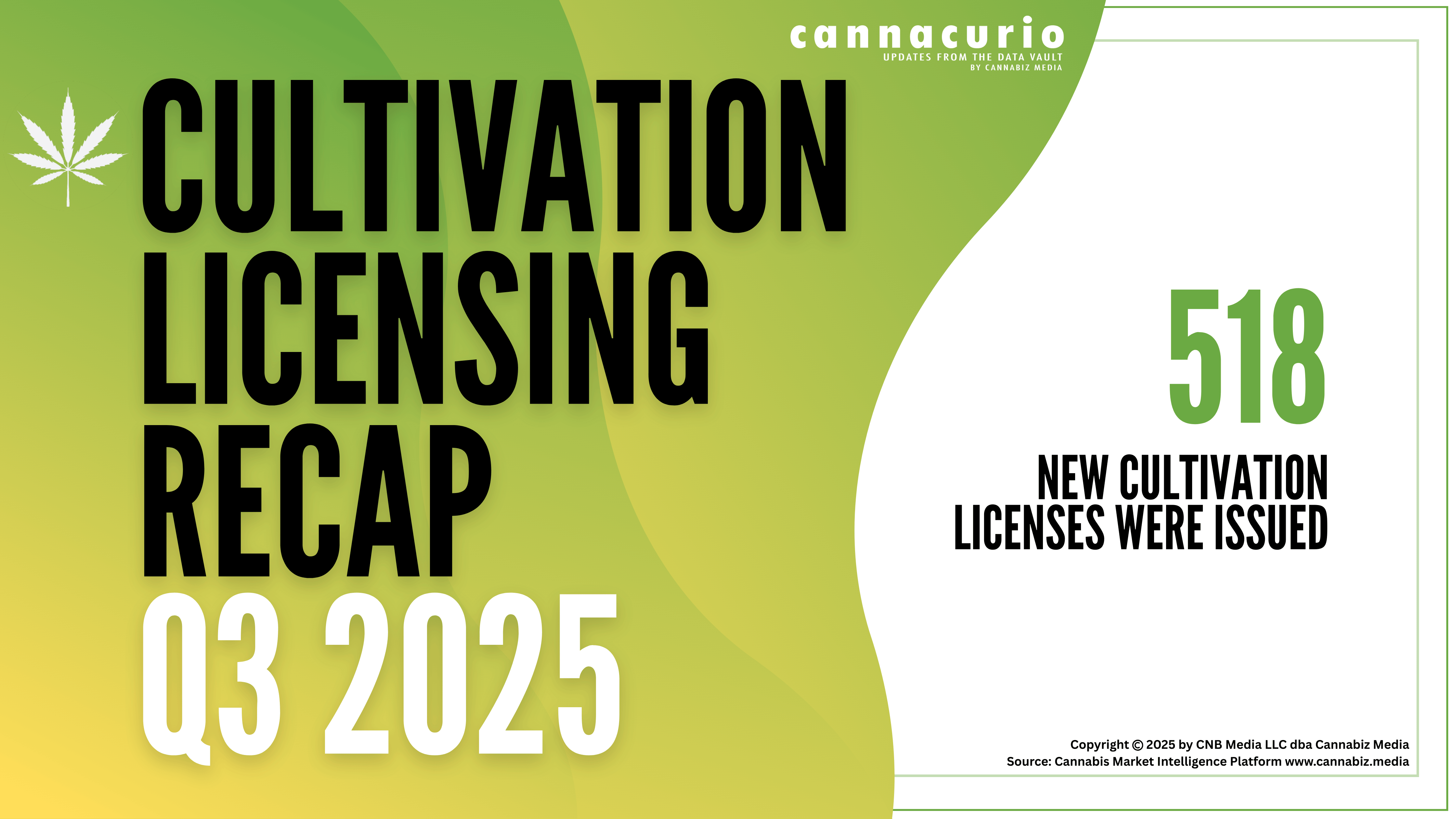

Cannabis M&A and the Gartner Hype Cycle

Tracking mergers and acquisitions (M&A) in any emerging business ecosystem is always interesting. It allows you to see the madness of early-stage growth markets and the many ups and downs that are experienced before reaching market maturity. The cannabis industry has definitely experienced significant fluctuations in terms of M&A activity, as should be expected in an emerging industry.

Fortunately, Cannabiz Media closely monitors cannabis M&A activity and summarizes this activity in a variety of dashboards and reports. Their dataset includes M&A activity in both the United States and Canada for licensed cannabis businesses, ancillary cannabis companies as well as equivalent companies in the hemp industry.

At the CannaTech Group, we serve as advisors on cannabis technology, which puts us at the intersection of two industries - the emerging cannabis industry as well as the more-established technology industry. From that vantage point, we saw an interesting connection between the two - the Gartner Hype Cycle.

The idea of the Hype Cycle is to describe five distinct phases by which emerging technologies reach maturity. The big takeaway is that technologies do not mature in a steady, linear fashion but experience highs and lows along the way.

Mapping Gartner Hype Cycle Phases to Cannabis Industry M&A

Our insight was that Hype Cycle phases map fairly well to the highs and lows of M&A activity being experienced by the cannabis industry. Below, we have listed the five phases of the Hype Cycle and added our own thoughts for each phase vis-à-vis the cannabis category.

Innovation Trigger

The “madness” of California, Colorado, and other early states commercializing medical cannabis and then Colorado and Washington becoming adult-use legal, spurred a wave of cannabis entrepreneurship and innovation.

Interestingly, the first documented M&A transaction in the Cannabiz Media dataset occurred in California in 2016 when Terra Tech Corp. acquired Blum Oakland, a retail medical cannabis dispensary, for US$21M (Figure 1).

Peak of Inflated Expectations

Think 2019 and 2020 with a wave of new cannabis investors funding questionable business models and optimism about the likelihood of federal cannabis legalization. Much of the merger activity at the time was the consolidation of existing cannabis companies seeking to strategically achieve scale across multiple states.

One of the largest deals during this time closed on February 3, 2020 with Curaleaf, a prominent East Coast Multi-State Operator (MSO), acquiring Cura Partners. The US$949M deal gave Curaleaf control of the Select brand as well as three facilities and 12 licenses on the U.S. West Coast. The deal helped Curaleaf move closer to its 2023 national license footprint shown in the map in Figure 2, also taken from the Cannabiz Media database.

Trough of Disillusionment

This is the down round we are currently experiencing in the cannabis space, with established U.S. state cannabis markets no longer growing, new adult-use states ramping up much slower than expected, and no progress with federal legalization.

From an M&A perspective, this trough creates another potential wave of buy/sell opportunities. We are currently speaking with investors looking to acquire distressed cannabis companies and assets via acquisitions and debt. No one probably wants to be called a bottom feeder, but it’s a thing!

Slope of Enlightenment

This will likely occur in 12- to 24-months as the cannabis markets and broader financial markets adjust and more states come online for adult-use.

Plateau of Productivity

Reflecting market maturity, this phase is likely still many years away and will happen after adult-use is made federally legal in the US and a true national cannabis market is created.

Another Landscape View

Alan Brochstein, CFA, is the founding partner of New Cannabis Ventures, a well-respected cannabis investor site. He offered the following insights that closely align with the early phases of the Gartner Hype Cycle.

“I feel like investors, companies, everybody in the media especially got overjoyed when Biden and Harris were elected. Cannabis stocks shot up to a recent high in February 2021, right after that, and people were expecting big things, even though big things weren’t very likely to happen and what they were counting on happening wouldn’t have mattered that much. So, from my perspective, we are in a terrible business climate in terms of price competition. And we can go into the reasons, many reasons, including some things that are not common to other industries, like the illicit market.”

Brochstein closed with two important points.

- Will cannabis companies that grow, process or sell cannabis ever be able to trade on the New York Stock Exchange or the NASDAQ? Right now, it's not illegal, but those exchanges don't permit it if they're American [companies] because of the federal legality.

- More important than that, 280E is causing a big problem right now. It was created by the IRS in the Nixon administration to penalize cocaine traders. And the idea was, if you make money illegally, your tax rate is on not your profits, but on your gross profits. And so, your operating expenses are no longer deductible. Well, I don't think that cannabis should be considered like that, but it is a Schedule I drug. There's a lot that could happen if they change it from Schedule I to something lower, some of it good, some of it bad, but the 280E tax eats up cash or makes cash really hard to get. Yeah – changes in 280E will certainly impact M&A and valuations.

The Numbers Don’t Lie

There are different ways to slice/dice and view M&A data. Instead of a single snapshot in time, looking at M&A activity over time is more interesting. In Figure 3 below, you have eight years of quarterly cannabis M&A activity that show the number of tracked transactions as well as the total deal value.

From modest activity starting in 2016, Q1-2019 and Q1-2020 were both particularly active quarters, and the peak of M&A deal-making was reached over a few quarters in 2021 in the midst of COVID. In Q4-2021, there were 41 closed M&A deals that totaled US$3.26B! Then you can visually see how rapidly the M&A window closed in 2022 and beyond.

Which organizations remained active in M&A during 2022? The table in Figure 4 provides the answer, with Sundial Growers Inc. acquiring the most cannabis facilities (67), TerrAscend Corp. having the greatest deal value (US$573.5M), and PharmaCann acquiring the most licenses (122).

Conclusion

Where cannabis M&A activity in 2019 and 2020 was mostly driven by industry optimism and an influx of new capital entering the cannabis space, activity in 2023 and into 2024 will be driven by distressed, cash-poor companies being acquired by opportunistic buyers who have deeper pockets or who have done a better job of preserving cash during the Trough of Disillusionment.

The long-term outlook for the cannabis industry is still bright, but with additional time needed for new East Coast adult-use markets to reach full operation and U.S. federal laws to become more favorable to cannabis, the Slope of Enlightenment and Plateau of Productivity are still years away.

About the Authors

Harry Brelsford is a principal analyst at The CannaTech Group, Paul Seaborn is an Assistant Professor in the McIntire School of Commerce at the University of Virginia.

.png)